PUBLISHED: 9th October 2020

The ACA and GINA work together for the hereditary cancer community

Members of our community frequently have questions about the laws protecting people with hereditary cancer and inherited genetic mutations. Often, there are also misunderstandings about the definition of a pre-existing condition. Here, we clarify what is considered a pre-existing condition and the primary U.S. laws that protect people affected by hereditary cancer.

Key laws related to genetic discrimination and health care

FORCE was a significant player in the passage of Genetic Information Nondiscrimination Act (GINA) in 2008, which prohibits health insurance companies and employers from discriminating against people based on a genetic or inherited predisposition to any disease, including cancer. The law also bars employers from asking employees to reveal personal or relatives’ health or genetic information, and from using genetic information when making hiring, firing, job assignment, or promotion decisions.

The Patient Protection and Affordable Care Act (ACA) significantly expanded health insurance availability and consumer protections for Americans. The law contains several components that benefit people affected by cancer. Notably, the ACA bans the practice of charging more or denying health insurance coverage due to a pre-existing health condition. Before the ACA was implemented, some health insurers were allowed to charge people with a pre-existing condition higher health insurance premiums—or to deny a policy altogether. The ACA also guarantees coverage of certain preventive health services, protects people enrolled in clinical trials, and prohibits health plans from putting annual or lifetime dollar limits on most benefits, and more.

What is a pre-existing condition and how can it be used?

A pre-existing condition is typically a “manifest” or existing disease/condition such as diabetes, colitis or a cancer diagnosis. A disease typically is considered manifest at the point when a doctor can diagnose the disease based on symptoms.

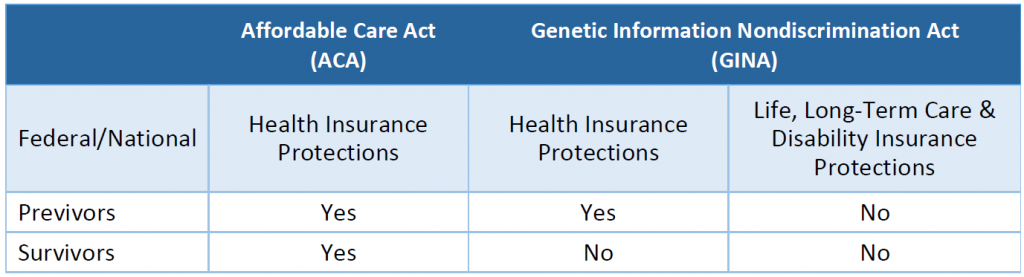

A major misconception is that a person with an inherited gene mutation linked to cancer risk but no cancer diagnosis (also known as a previvor) is considered a person with a pre-existing condition for health insurers. This is not accurate. In fact, GINA prohibits treating genetic information or a family history of disease as a pre-existing condition when it comes to health insurance or employment.

Under GINA, a previvor with a BRCA, PALB2, CHEK2, Lynch syndrome or other mutation (who has not been diagnosed with cancer), does not have a pre-existing condition when it comes to health insurance. Even if the ACA is repealed, as long as GINA remains law, s/he cannot be charged a higher health insurance premium or denied a health insurance policy based on the mutation or family history alone.

On the contrary, a genetic mutation carrier with any type of cancer has a manifest disease, which is considered a pre-existing condition. The ACA currently protects this person from health insurance discrimination, but because the individual has had cancer, s/he is not protected by GINA.

Table 1- Pre-existing condition protections

In summary, regarding health insurance, GINA protections only apply to genetic information for previvors (aka unaffected carriers) who have not been diagnosed with the related disease. Once a person receives a diagnosis such as cancer, it is considered manifest disease. Manifest disease is not protected under GINA.

GINA loopholes and exceptions

It is important to note that GINA does not apply to life, long-term care or disability insurance. It is legal for an insurer to deny these types of insurance to previvors with BRCA or other inherited genetic mutations without manifest disease. Some states have stronger laws that prohibit genetic discrimination by these insurers. Also, some insurers choose not to take advantage of this “legal discrimination” option but we encourage people who are denied a policy to explore other insurers if possible.

The ACA complements GINA

The term manifest disease is not always straightforward. For example, before someone has a full-blown disease, s/he may have signs or symptoms that relate to being high-risk. Pre-diabetes or colon polyps could be examples where protections under GINA may be fuzzy. This is why the Affordable Care Act, which prohibits discrimination for any predisposition to or manifest disease is so important to our community; the ACA closed the health insurance gaps that remained after the passage of GINA.

If the Affordable Care Act is repealed or replaced at some point, health insurers may be allowed to raise health insurance premiums or deny policies for people with a diagnosis of a condition such as cancer, diabetes, high blood pressure, or even a prior surgery or injury. This is why FORCE and our partners in patient advocacy community strongly support the pre-existing condition protections in the ACA. The law is not perfect, as there are some provisions in the ACA that need revisions and improvement, but the basic protections it provides are essential. FORCE continues to advocate in support of legislation and public policies that protect all members of our community and provide access to affordable, quality health care.